Featured

Table of Contents

Exact same $18,000 at 12% APR on an individual loan, same $540/month payment = 3.2 years, $2,800 in interest. The most common combination mistake: take out the loan, zero the cards, then run the balances back up to $12,000 within 18 months.

If your costs practices have not changed, the loan will not fix anything it just reprices the issue. Moving from 680 to 740 can cut your APR by 58 points on the exact same loan.

Lenders desire overall monthly debt payments listed below 40%43% of gross earnings. If you're currently at $2,400 in responsibilities, a $400/month loan payment disqualifies you before lenders even run your rating.

Understanding Debt-Relief Counseling for 2026

Take the much shorter term if you can handle it. brings a real rates penalty. Self-employed borrowers frequently get estimated 25 points greater than employed employees with the exact same rating. Have 2 years of federal tax returns and a profit-and-loss statement ready. A 720+ FICO at LightStream or SoFi partly offsets the income-verification surcharge.

That's the tradeoff. If you own a home, a home equity loan or HELOC will practically always beat an individual loan on rate. With 30-year set home loan rates presently running 6.5%7.0% per Federal Reserve tracking, home equity products are landing in the 7%9% variety and that interest may be tax-deductible under internal revenue service rules if you use it for home enhancements.

Ally Bank and many credit unions offer this. If you have $10,000 in an Ally cost savings account earning 4.5%5.0% APY and need to obtain $8,000, a protected loan using that account as collateral can price listed below an unsecured loan and your cost savings keeps making interest the entire time. Default on it and you lose the account.

Ways to Choose the Top Certified Credit Advisory

These five moves produce genuine, measurable outcomes: One in 5 Americans carries an error per the FTC. Conflict errors at the only federally mandated free source. A fixed error can add 2040 points within 60 days at zero expense. Each difficult query drops your score 35 points. SoFi, Marcus, and LightStream all use soft-pull pre-qualification.

FICO weights credit utilization at 30% of your rating. Dropping from 65% to under 30% utilization can add 3050 points in a single billing cycle.

The co-signer is fully accountable if you miss payments make sure they understand that before finalizing. Updates from paying for a card or having a negative mark age off take 3060 days to reflect in your file. Apply prematurely and you're paying for a rating that's already on its method up.

Securing Low-Interest Personal Loans in 2026

At 15% APR on $18,000 over 48 months, you'll pay about $5,930 in interest. Keeping the very same debt on cards at 23% with an identical reward timeline expenses approximately $11,400. That's a $5,470 difference for submitting one application. Lock in the lower rate, stop using the cards, and do not reopen them till the loan is paid off.

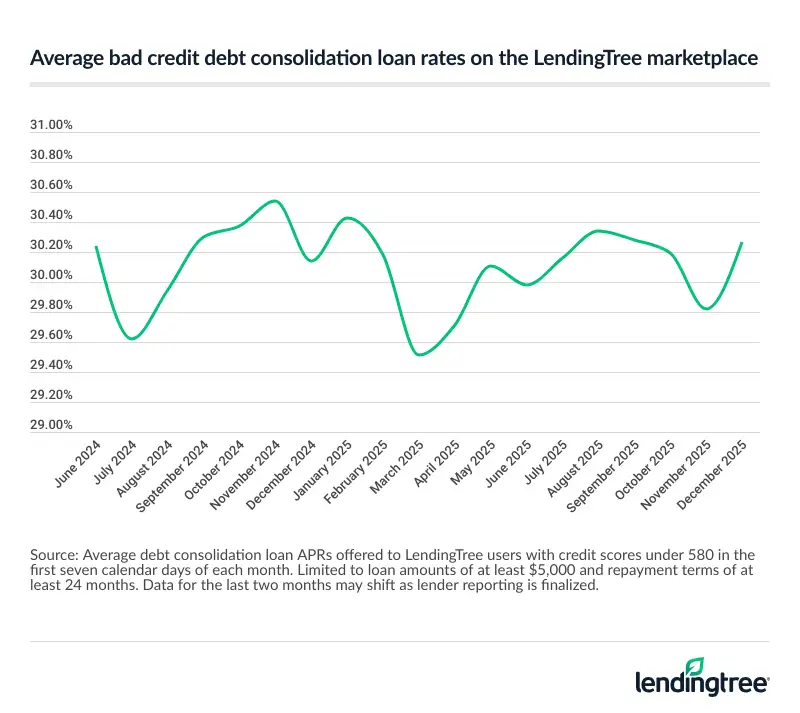

LendingClub, Avant, and Upgrade all work with scores in the 580650 range, but expect APRs of 22%30%. On a $10,000 loan at 28% over 36 months, you're paying $4,600 in interest total. That's steep, but it still beats keeping $10,000 on a card at 24% APR and paying minimums for five years.

Exact same FICO, same earnings, exact same loan two models, two rates. The spread between loan providers on the very same debtor consistently runs 35 points, which on a $15,000 loan over 36 months is $1,300$2,200 in interest.

Key Steps for Reducing Interest Payments Via Management

Above 10%, pay it off getting rid of high-rate debt is an ensured return that beats the S&P 500's 10% historic average on a risk-adjusted basis. Listed below 7%, the mathematics moves towards investing, especially inside a Roth IRA (2026 limit: $7,500/ year). Between 7%10%, it's really close most people sleep much better killing the financial obligation.

Bring 2 years of federal tax returns (Arrange C) and a profit-and-loss declaration. If your rating is under 700, three months of targeted improvement before applying will likely save more than rushing to use now.

Utilize our free to compare any mix of amount, APR, and term side by side before you sign anything. See:.

It's all structured, every step of the method. Examining your rate takes just a couple of minutes. From there, as soon as you choose the loan you wish to move forward with, the application takes just a few minutes. Most consumers get a same-day choice. Once you're approved, you could receive funds as quickly as the exact same day you sign for your loan.

A little loan from LendingClub Bank is a fixed-rate personal loan that can assist you get precisely what you need to pay down high-interest debt or cover your expenses now while keeping your month-to-month payment the very same for the duration of your repayment strategy. A little individual loan can start as low as $1,000 and offers competitive rates.

Using Online Loan Calculators to Manage Finances

Borrow a small amount, just what you needQuick and easy online applicationEligibility based upon credit historyFunded in as little as 24 hoursNo prepayment costs.

A small loan from LendingClub Bank is a fixed-rate personal loan that can help you get exactly what you need to pay down high-interest debt or cover your expenses now while keeping your month-to-month payment the exact same for the duration of your repayment strategy. A small individual loan can start as low as $1,000 and offers competitive rates.

Obtain a percentage, just what you needQuick and simple online applicationEligibility based upon credit historyFunded in as little as 24 hoursNo prepayment charges.

Official Housing and Financial Counseling in 2026Editorial Note: Intuit Credit Karma receives compensation from third-party advertisers, however that doesn't impact our editors' opinions. Our third-party advertisers do not evaluate, approve or endorse our editorial content. Information about financial items not offered on Credit Karma is gathered individually. Our material is accurate to the very best of our knowledge when published.

{kind=link}

Latest Posts

Comparing Affordable Personal Financing in 2026

Analysing Proven Credit Options in 2026

Strengthen Credit Health With Proven Education